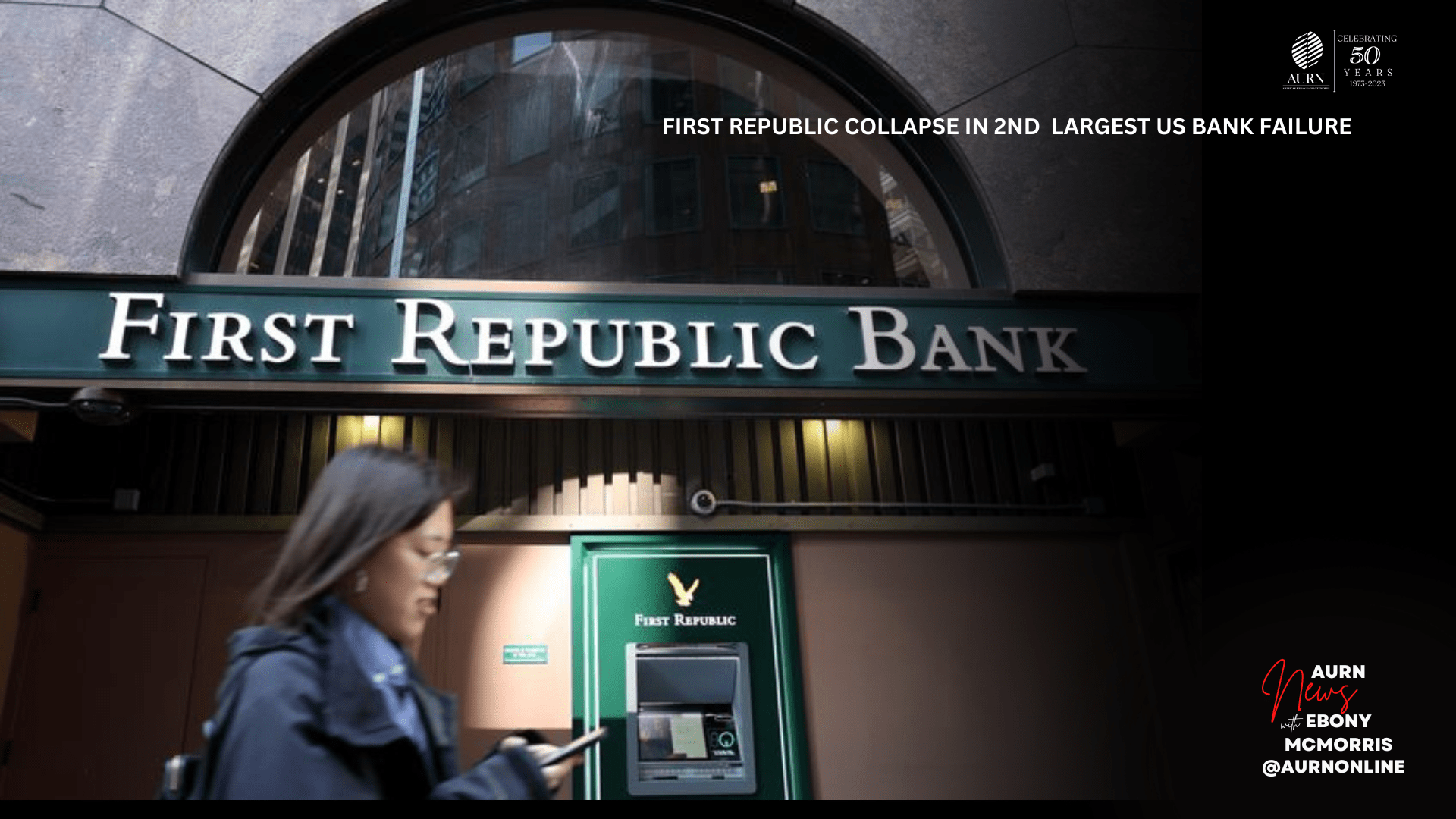

First Republic Bank, the embattled California lender, has collapsed in the second-largest bank failure in U.S. history. Regulators have orchestrated an overnight deal, with JPMorgan Chase acquiring most of the bank’s assets and deposits.

The Federal Deposit Insurance Corporation (FDIC) and California regulators simultaneously closed First Republic Bank and sold off all $93.5 billion of its deposits and most assets to JPMorgan.

The U.S. Treasury Department expressed confidence in the safety of deposits and the resilience of the banking system. The development follows last month’s collapse of Silicon Valley Bank and Signature Bank, triggering deposit runs and widespread panic among similar institutions.

As this dramatic turn of events unfolds, two critical questions must be asked: What measures can be taken to prevent future large-scale bank failures? And can the U.S. banking system swiftly recover from this series of collapses?

Click play to listen to the report from AURN White House Correspondent Ebony McMorris. For more news, follow @E_N_McMorris & @aurnonline.